Wall Street drifted in mixed-to-lower trading on Monday, with major indices closing slightly in the red. Following the Federal Reserve's decision to cut rates by 25 basis points last week, investors have entered a period of observation. Markets are now bracing for key economic data due this week, including payrolls and inflation reports, to gauge the policy trajectory for 2026. Continued valuation pressure on tech giants and shifting geopolitical narratives also shaped the day's sentiment.

Market Overview

Global & Regional Context

Global markets showed a split performance. European equities generally rose on improved export outlooks, while Asian markets slumped due to concerns over slowing growth in the tech supply chain. In the FX market, the US dollar saw a modest rebound after sessions of weakness but remained within its recent range.

Local Market Performance

The major US indexes stayed within tight ranges as the market sat in a "data vacuum" ahead of key reports.

- Dow Jones Industrial Average: Fell 41.49 points, or 0.1%, to 48,416.56.

- S&P 500 Index: Slipped 10.90 points, or 0.2%, to 6,816.51.

- Nasdaq Composite: Dropped 137.76 points, or 0.6%, to 23,057.41, significantly weighed down by large-cap tech.

Sector Highlights

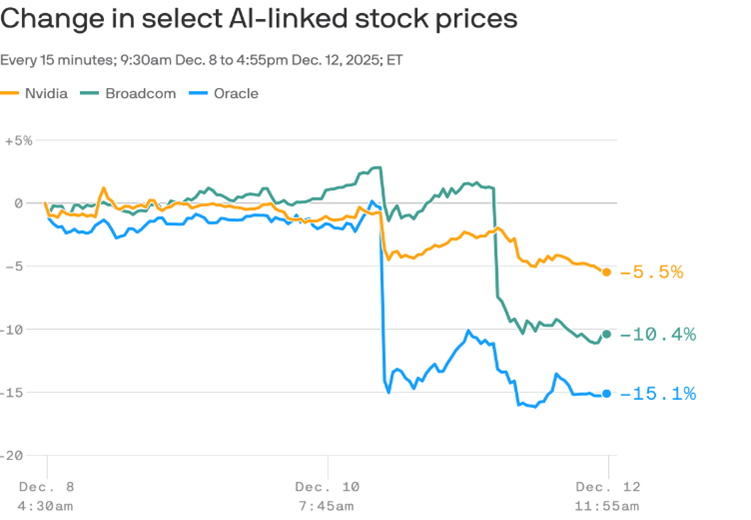

Tech & AI (Growth Pressure)

The technology sector, particularly semiconductors, continued to face headwinds. Broadcom (AVGO) declined following a price-target cut from analysts, sparking debates over whether the peak of AI hardware spending has been reached. Meanwhile, lingering effects from Oracle's previous revenue miss dampened appetite for software stocks.

Biotechnology Standouts

Despite the broader weakness, the biotech sector provided some bright spots. Kyverna Therapeutics (KYTX) saw its shares soar on breakthrough clinical data, drawing investor interest back to innovative drug pipelines.

Defensive & Consumer Rotation

Sentiment tilted toward defensives. Consumer staples like Hershey (HSY) bucked the trend following analyst upgrades. Conversely, some retail giants like Costco (COST) lagged due to concerns over softening fundamentals.

Stocks to Watch (For Market Observation Only — Not Investment Advice)

| Stock | Symbol | Reason for Interest |

|---|---|---|

| Kyverna Therapeutics | KYTX | Shares surged over 30% following positive Phase 2 data for its treatment of Stiff Person Syndrome (SPS). |

| Broadcom | AVGO | Pressured by analyst downgrades and growing caution regarding the sustainability of AI infrastructure growth. |

| Hershey | HSY | Gained on an upgrade highlighting earnings visibility, showcasing strong defensive qualities in a volatile market. |

Market Drivers

- Interest Rate Outlook: While the Fed cut rates on Dec 10, the "hawkish" undertone has left investors worried about limited easing in 2026.

- Tech Valuation Reset: After massive year-to-date gains, investors are re-evaluating the ROI timelines for AI leaders relative to their high valuations.

- Geopolitical Dynamics: Latest updates on the Middle East situation (including reports of strike delays) helped stabilize oil prices but caused fluctuating safe-haven flows.

- Economic Data Anticipation: Markets are holding their breath for Tuesday's labor data and upcoming CPI reports to confirm the "soft landing" narrative.

Outlook

Analysts anticipate that US markets will remain range-bound for the remainder of the year. Market leadership may continue to rotate from high-growth tech toward value and defensive sectors. A key technical watchpoint is whether the S&P 500 can hold the 6,800 level, which will determine if a "year-end rally" can materialize following this week's data catalysts.