On Monday, November 10, 2025, the international oil market exhibited a cautious, range-bound movement with a bearish undertone. Despite a rebound in global demand during Q3 fueled by an improving macroeconomic climate, persistent inventory builds and robust non-OPEC+ supply growth weighed on sentiment. Investors remained on the sidelines, awaiting clearer signals regarding OPEC+ production policy and the fading of geopolitical risk premiums.

Market Overview

Global Context

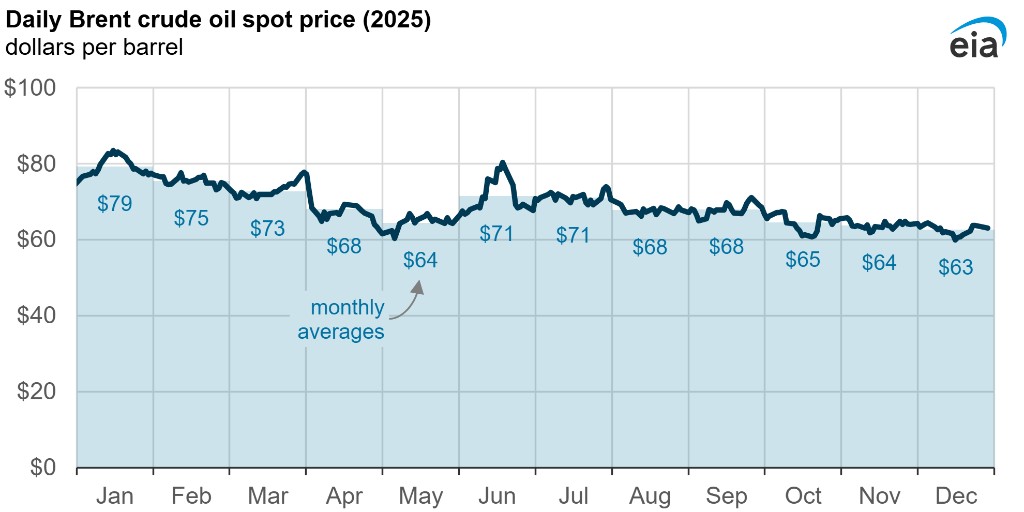

As of November 10, benchmark crude prices remained within a downward consolidation channel. According to the latest IEA data, while global demand growth recovered to 920 kb/d in 3Q25 (led by stronger deliveries in China), the overall market was dampened by high global stock levels. Additionally, a strengthening U.S. Dollar exerted downward pressure on dollar-denominated crude futures.

Key Price Reference

- Brent Crude: Hovering around $62.00 - $64.00/bbl.

- WTI Crude: Trading in a narrow range between $58.00 - $60.00/bbl.

Market Highlights

Supply-Side Dynamics

OPEC+ Dilemma: Markets were pricing in the potential for production increases or quota adjustments from OPEC+ (led by Saudi Arabia) heading into December. While the group maintained cuts in early November, record output from non-OPEC+ producers (US, Brazil, Guyana) continued to offset these efforts.

Shale Resilience: U.S. shale production remained steady, further challenging OPEC's ability to defend price floors.

Demand-Side Divergence

The China Factor: Easing trade tensions bolstered demand for petrochemical feedstocks and transport fuels in China, serving as a critical support level for prices.

Energy Transition Impact: The rising adoption of electric vehicles continued to structurally decelerate gasoline demand growth, a trend increasingly reflected in November's market sentiment.

Refining and Inventories

Margin Rebound: Refining margins in Europe and Asia reached a two-year peak in early November due to unplanned outages and maintenance, temporarily boosting physical crude demand.

Domestic Policy: On November 10, China's NDRC announced a new adjustment to retail fuel prices, reflecting the recent volatility in international crude costs.

Market Drivers and Indicators

| Driver | Status | Impact Description |

|---|---|---|

| Global Demand Growth | Gradual Recovery | 3Q25 growth doubled from 2Q25 but remains below historical averages. |

| Inventory Levels | Persistent Builds | Global stocks in late 2025 grew at the fastest pace since 2020. |

| OPEC+ Policy | Watchful/Divided | Market fears potential supply increases after December. |

| Macro Environment | Rate Cut Expectations | Improving economic outlooks from anticipated rate cuts support industrial demand. |

Outlook

Analysts expect oil prices to continue bottoming out within the $60 - $70 range for the remainder of 2025. While geopolitical events may cause short-term spikes, the overarching theme of oversupply (with an implied stock build of nearly 2.5 million b/d in late 2025) will likely cap any significant upside rallies.