On Monday, December 15, 2025, the international oil market exhibited significant weakness, with prices breaking below key psychological support levels. Although major agencies slightly adjusted demand forecasts, a massive surge in global inventories—rising at the fastest pace in late 2025 since the 2020 pandemic—fueled bearish sentiment for the 2026 outlook. Both WTI and Brent crude closed lower as the market struggled with relentless production growth from non-OPEC+ nations.

Market Overview

Global and Regional Context

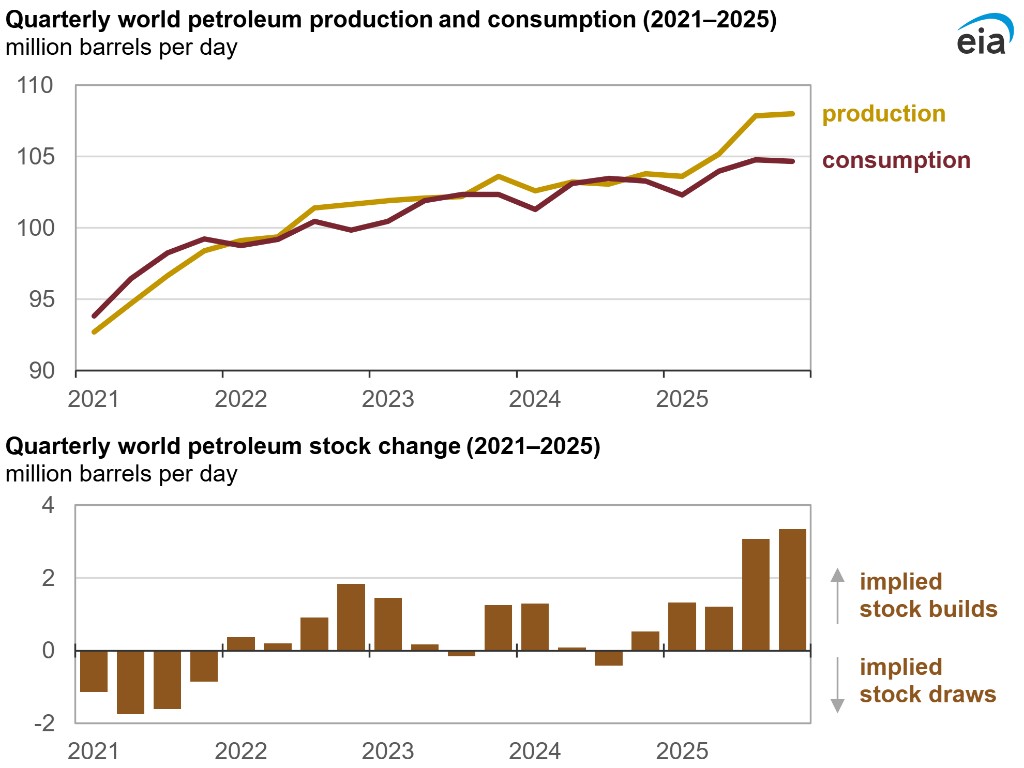

By mid-December, the narrative of a global supply glut was firmly established. According to the latest monthly reports from the IEA and EIA, implied stock builds reached approximately 2.5 million b/d in the final quarter of 2025. The continued expansion of U.S. shale, alongside output gains from Brazil and Guyana, effectively neutralized OPEC+ efforts to stabilize the market through production cuts.

Core Price Performance (Closing Dec 15)

- Brent Crude: Fell approximately 0.9%, trading around $59.50 - $61.20/bbl, with monthly averages hitting their lowest since early 2021.

- WTI Crude: Dropped 1.08% to settle at $56.82/bbl.

Market Highlights

Supply-Side Pressure

Inventory "Flood": December data showed observed global oil inventories rising by 37 million barrels. For the full year of 2025, total stock builds reached nearly 477 million barrels, leaving investors concerned about storage capacity.

Non-OPEC+ Dominance: Despite a slight dip in OPEC+ output in November due to outages in Kuwait and Kazakhstan, the market remained hyper-focused on record U.S. production, which has eroded the cartel's pricing power.

Demand Resilience vs. Structural Shifts

Refining Margin Spike: Paradoxically, while crude prices slumped, global refining margins hit three-year highs in early December due to limited capacity. This created a disconnect where refined products remained relatively expensive compared to the crude oil surplus.

Energy Transition: The increasing adoption of electric vehicles continued to structuralize the slowdown in gasoline demand growth. While 2025 saw a demand increase of 830 kb/d, much of this was driven by the petrochemical sector rather than transport fuels.

Macro and Geopolitics

Currency Impact: Fluctuating expectations for 2026 central bank policies led to a stronger U.S. Dollar, increasing the cost of oil for buyers using other currencies.

Fading Risk Premiums: Geopolitical tensions saw a marginal cooling in mid-December, further removing the "fear premium" that had previously supported prices.

Key Drivers and Indicators

| Driver | Status | Impact Description |

|---|---|---|

| WTI Closing Price | $56.82 | A 1.08% decline reflecting strong bearish sentiment. |

| Global Inventories | 4-Year High | Massive stock builds at the end of 2025 cap any potential for a price rally. |

| Refining Margins | Multi-year Peak | Product availability constraints supported margins despite the crude surplus. |

| 2026 Forecast | Oversupply | Non-OPEC+ supply is expected to grow by another 2.4 mb/d in 2026. |

Outlook

Analysts anticipate that oil prices will remain under pressure in early 2026 due to the high inventory base inherited from 2025. The market is now looking toward January trade data to gauge whether major importers like China will increase strategic stockpiling at these lower price levels, potentially providing a floor for the market.